When dealing with UK crypto exchange regulation, the set of rules that govern how digital asset platforms operate in Britain, covering licensing, consumer protection, and anti‑money‑laundering duties. Also known as British crypto compliance, it shapes everything from token listing to fee structures. Financial Conduct Authority (FCA) acts as the supervisory body, issuing licences and enforcing standards. Anti‑Money Laundering (AML) obligations form a core pillar, demanding robust KYC, transaction monitoring, and reporting. Finally, crypto exchange licensing ties the whole framework together, ensuring only vetted platforms can serve UK users.

The FCA requires every exchange that offers services to UK residents to be registered under the AML Regulations 2017. This means maintaining a risk‑based approach, conducting customer due‑diligence, and filing suspicious activity reports. In practice, exchanges must integrate real‑time AML screening tools, store audit logs for at least five years, and train staff on compliance. The licensing process also evaluates the platform’s governance structures, cybersecurity measures, and capital adequacy. A well‑structured compliance program not only avoids hefty fines but also builds trust with traders, which in turn drives liquidity and market depth.

Beyond AML, the UK introduced specific rules for Distributed Ledger Technology (DLT) under the FCA’s “crypto‑asset” regime. Tokens that qualify as “crypto‑assets” are split into three categories: security tokens, e‑money tokens, and exchange tokens. Security tokens fall under existing securities law, while e‑money tokens are treated like electronic money, subject to the Electronic Money Regulations. Exchange tokens, such as Bitcoin or Ethereum, are largely exempt from strict securities rules but still must meet AML standards. Understanding where a token sits in this taxonomy is essential for exchanges when designing listing criteria and disclosure policies.

Tax considerations add another layer. HMRC treats crypto gains as either capital gains or trading income, depending on the user’s activity. Exchanges therefore need to provide clear statements to users, outlining realized gains, cost bases, and any withheld taxes. Accurate reporting not only helps users meet their obligations but also reduces the risk of the platform being flagged for facilitating tax evasion. Many exchanges now offer integrated tax‑reporting dashboards, turning a compliance headache into a value‑added service.

Operational resilience is a non‑negotiable part of the UK framework. The FCA expects robust business continuity plans, regular penetration testing, and segregation of client funds. Failure to isolate user assets can trigger regulatory sanctions and erode confidence. Moreover, the UK’s open‑banking initiative encourages exchanges to adopt secure API standards for fiat on‑ramps, further tightening the safety net for users moving between traditional banks and digital wallets.

All these pieces—FCA oversight, AML duties, DLT classification, tax reporting, and operational safeguards—create a tightly woven compliance tapestry.UK crypto exchange regulation isn’t just a checklist; it’s a dynamic set of standards that evolve with market innovation. Below you’ll find a curated collection of articles that break down each component, from step‑by‑step licensing guides to deep dives on AML tech, helping you navigate the British crypto landscape with confidence.

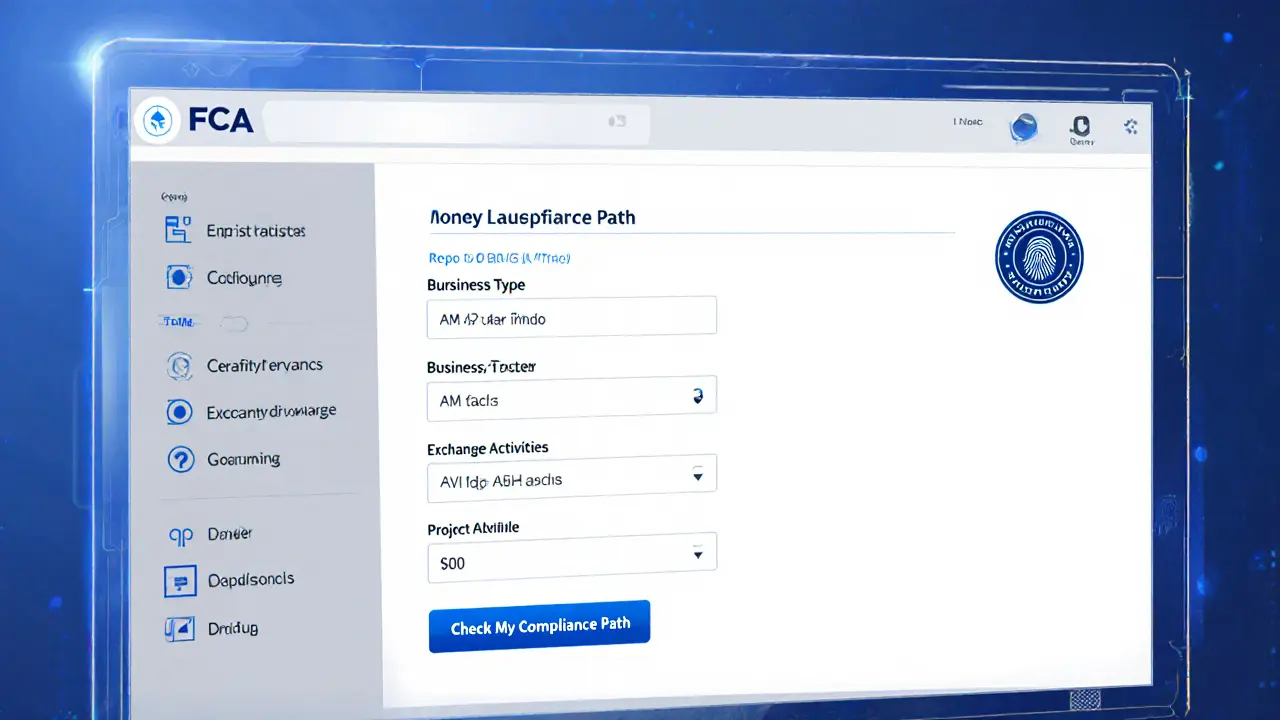

A practical guide to UK FCA crypto exchange authorization, covering current AML registration, upcoming FSMA licensing, territorial rules, stablecoin specifics, compliance checklist, and FAQs.

Tycho Bramwell | May, 28 2025 Read More