As of 2026, there is no single set of rules for cryptocurrency in the United States. Instead, each state has built its own system - and they couldn’t be more different. If you're running a crypto business, trading digital assets, or even just holding Bitcoin, where you live matters more than you think. One state might welcome you with open arms. Another could make it nearly impossible to operate without spending hundreds of thousands on legal fees. This isn’t theory. It’s reality.

Why State Rules Matter More Than Federal Ones

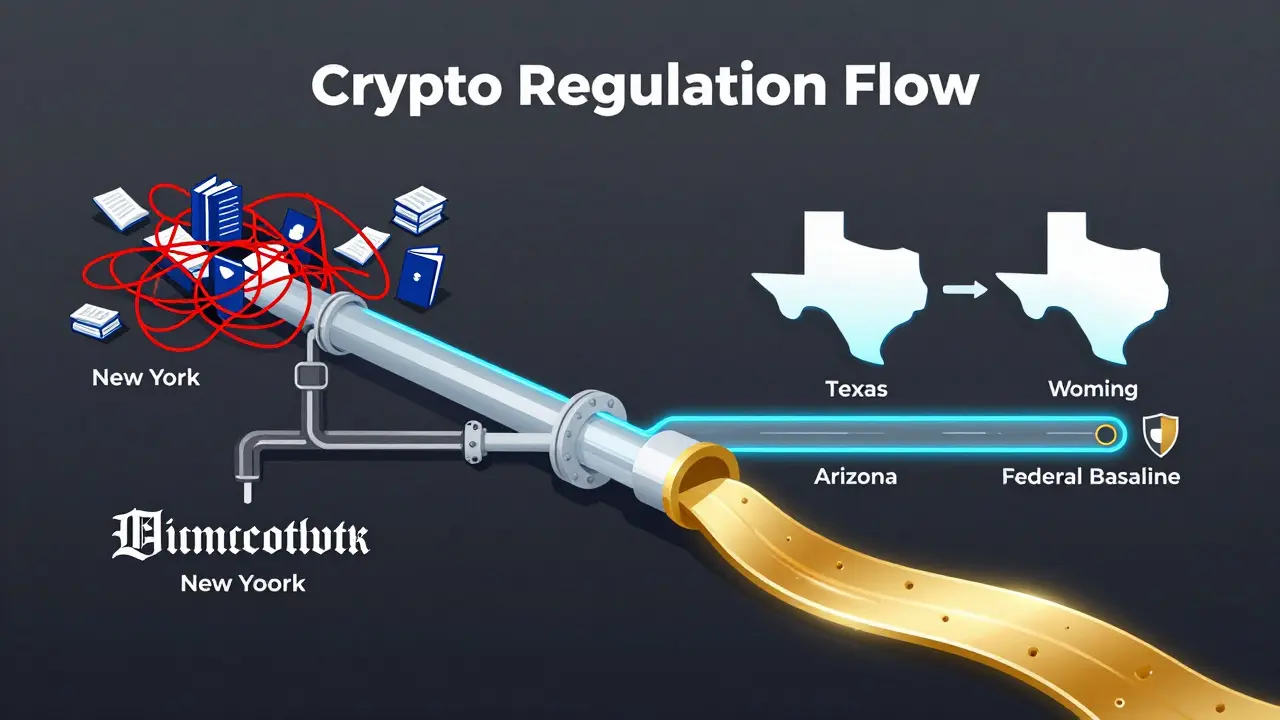

For years, the federal government stayed out of the way. The SEC said crypto was a security. The CFTC said it was a commodity. The IRS treated it like property. No one took clear charge. So states stepped in. By 2025, 47 out of 50 states had passed some kind of crypto law. The federal government finally moved with the GENIUS Act in September 2025, but even that didn’t override state rules - it just set a baseline. States still get to add their own layers.This patchwork system creates real problems. A company based in California can register in 60 days. The same company trying to operate in New York spends over a year and $350,000 just to get licensed. Many just pack up and move. That’s not a coincidence. It’s a direct result of how each state chose to regulate.

New York: The Hardest State to Operate In

New York’s BitLicense, launched in 2015, was the first major state-level crypto rule. It was meant to protect consumers. But it ended up acting like a wall. To get a BitLicense, you need:- $5,000 application fee

- $2 million in minimum net capital

- 24/7 cybersecurity monitoring

- 80% of crypto assets stored in NYDFS-approved cold wallets

- Biometric access controls for vaults

- Monthly compliance reports

- An onsite inspection every 12-18 months

The process takes an average of 14.3 months. Only 37 companies have ever been approved - out of over 100 applications. Coinbase, Circle, and others left New York years ago. Why? Because the cost of compliance eats up 25% of their budget. One exchange owner on Reddit said he spent $187,000 on compliance in NYC - and made zero revenue. He moved to Wyoming and tripled his business in 18 months.

For users, the downside is slower service. New York’s average time to resolve a crypto complaint? 217 days. That’s over seven months. Compare that to California’s 38% faster resolution rate.

Wyoming: The Crypto-Friendly State

Wyoming didn’t just make crypto rules - it built a whole new banking system for it. In 2018, it created Special Purpose Depository Institutions (SPDIs). These are state-chartered banks that can hold crypto as deposits. They’re insured by the FDIC. They can lend, custody, and trade digital assets - all under one roof.There are 12 crypto banks now operating in Wyoming. Kraken Bank and Avanti Financial Group are two big names. In 2024, these institutions handled $12.7 billion in crypto transactions. Why? Because the rules are clear:

- $25 million minimum capital

- FDIC insurance for crypto deposits

- No state income tax

- Exemption from money transmitter licensing

- Legal recognition of crypto as property

Wyoming doesn’t just attract businesses - it attracts talent. Since 2020, 63% of all new crypto banking jobs in the U.S. have been created in Wyoming. The state pulled in $427 million in revenue from crypto in 2024 - 7.3% of its total state income. That’s more than New York, despite having a population 1/50th the size.

California: The Middle Ground

California took a different approach. Instead of a full license, it created a registration system. If your company does more than $500,000 in crypto transactions per year, you must register with the Department of Financial Protection and Innovation (DFPI). The fee? $1,000. The process? 45 to 60 days.As of Q3 2025, 142 crypto businesses are registered in California. That’s more than any other state except Texas. It’s not perfect - the DFPI has opened 17 enforcement actions against unregistered firms - but it’s far less burdensome than New York. Companies like Coinbase and Coinbase Prime operate out of California because it’s practical. You can scale without going broke.

Users benefit too. Disputes get resolved 38% faster than in New York. And since California has strong consumer protection laws, users have legal recourse if something goes wrong.

The States You Should Avoid

Not all states are created equal. Some have rules so vague or so strict that they scare off innovation. Here are three to watch out for:- New York - High cost, slow approvals, no room for growth

- Massachusetts - Secretary William Galvin called the state-by-state system a "recipe for disaster." He’s cracked down hard on scams, but the rules are unclear for legitimate businesses.

- Connecticut - Requires bonding up to $500,000 and has no clear definition of what counts as "money transmission."

These states have seen net outmigration of crypto firms. Companies don’t just leave - they take jobs, tax revenue, and innovation with them.

The States That Are Winning

Beyond Wyoming, other states are making smart moves:- South Dakota - No state income tax, clear crypto definitions, and low fees. Attracted 3 new crypto banks in 2024.

- Tennessee - Passed a "Crypto Friendly Act" in 2024. Exempts individuals from licensing if they’re not running a business.

- Arizona - Created a regulatory sandbox. Startups can test products without full licensing. Result? 34% faster growth in crypto startups than in non-sandbox states.

- Texas - No state income tax. Only requires a basic cybersecurity plan. No bonding needed unless you handle over $1 million annually.

These states aren’t just attracting businesses - they’re building ecosystems. They’ve hired crypto lawyers, trained state regulators, and partnered with industry groups. They know this isn’t a trend. It’s the future of finance.

What You Need to Know If You’re a Business

If you’re running a crypto exchange, wallet service, or custody provider, here’s what to do:- Map your operations - Where are your servers? Where are your users? Where is your legal entity registered?

- Check licensing requirements - Some states require a license. Others just need registration. Some have no rules at all.

- Calculate compliance costs - New York: $350,000/year. Wyoming: $42,000/year. California: $85,000/year. The difference is huge.

- Consider relocation - If you’re stuck in a high-cost state, moving might be the smartest business decision you make.

Most companies now operate out of 1-3 states max. Why? Because managing 47 different rulebooks is impossible. A 2025 survey of 217 crypto firms found 68% said state regulatory uncertainty was their biggest challenge. 41% said they avoid certain states entirely.

What You Need to Know If You’re a User

If you’re just holding or trading crypto, your state still affects you:- Exchange access - Some platforms won’t let New York residents trade certain tokens.

- Withdrawal speed - New York users wait longer for withdrawals due to compliance delays.

- Consumer protection - California and Wyoming offer clearer dispute processes. New York? Not so much.

- Tax treatment - Wyoming and Texas don’t tax crypto gains. New York does. That’s a real difference in your wallet.

Even if you’re not a business, where you live shapes your crypto experience. Choose your exchange wisely. Don’t assume all platforms work the same everywhere.

The Future: Federal vs. State

The GENIUS Act of 2025 tried to bring order. It says stablecoins must be backed 100% by liquid assets. It gives the CFTC primary oversight. But it doesn’t take away state power. In fact, 22 states are now suing the federal government, claiming the Act violates the 10th Amendment.So what’s next? Experts predict one of two outcomes by 2028:

- Harmonization - Federal rules become the standard, and states align.

- Coexistence - States keep their rules, but federal rules set a floor. No state can be worse than federal minimums.

Right now, it’s chaos. But the market is already adapting. Companies are moving. Users are voting with their wallets. And states that make it easy are winning.

Which states have the strictest crypto regulations?

New York has the strictest rules, thanks to its BitLicense system. Massachusetts and Connecticut are also highly restrictive, with unclear definitions and high bonding requirements. These states prioritize enforcement over innovation, making it difficult for businesses to operate without heavy legal and compliance costs.

Can I avoid crypto regulations by operating online?

No. If you’re serving customers in a state with crypto regulations - even if your company is based elsewhere - you still have to comply. States use the "targeting" rule: if you market to, accept payments from, or have users in that state, you’re subject to its laws. Ignoring state rules can lead to fines, lawsuits, or being blocked from operating.

Is Wyoming the only state that allows crypto banks?

Wyoming was the first and remains the most developed, but other states are catching up. South Dakota and Nevada have introduced similar frameworks, and Tennessee is exploring state-chartered crypto institutions. However, only Wyoming has fully implemented and scaled the Special Purpose Depository Institution (SPDI) model with FDIC insurance and clear legal protections.

Do I need a license to hold Bitcoin as an individual?

No. No state requires individuals to get a license to buy, hold, or sell Bitcoin for personal use. Regulations only apply to businesses that transmit, store, or exchange crypto on behalf of others. If you’re just holding crypto in your own wallet, you’re not regulated.

What happens if I move from New York to Wyoming?

If you’re a business, you’ll likely save over $250,000 a year in compliance costs and cut your licensing time from over a year to under six months. If you’re an individual, you’ll benefit from no state income tax, faster access to crypto services, and fewer restrictions on trading. Many businesses have relocated for these exact reasons - and seen growth as a result.